The meme that is destroying Western civilisation—Part III

Yesterday’s UK election has repeated the pattern of the last 40 years: a Neoliberal-Heavy Party—the Conservatives—have lost in a landslide to a Neoliberal-Lite Party—Labour. The victor will set about implementing the same economic policies as the party it routed, but more nicely.

Jeremy Corbyn—the previous anti-Neoliberal leader of the Labour Party, who held onto his seat as an independent, after Labour’s current pro-Neoliberal leader Kier Starmer banned him from standing for Labour—put the election result in context when he commented that Labour “has put forward a manifesto that is thin to put it mildly, and doesn’t offer a serious economic alternative to what the Conservative government is doing.”

The root problem, as I noted in my previous post (Substack;Patreon), is that both parties—and almost all of the bureaucracy, the media, and economic thinktanks, as a reader pointed out—have Neoliberalism “embedded in them”. They all think that Marshall’s meme of intersecting supply and demand curves describes how the real-world works. So, despite vast differences between political parties on issues like culture and immigration, when it comes to the economics, all you get is a different brand of the same old breakfast cereal.

It's the breakfast cereal that is the problem.

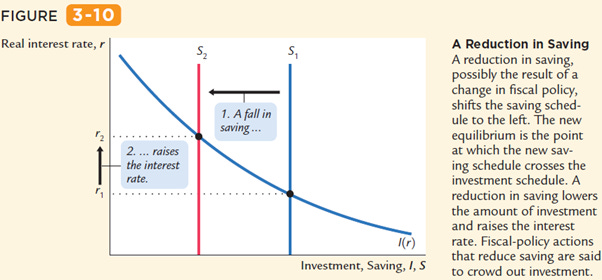

The easiest place to prove that supply and demand analysis is false is the area where its application does the greatest harm: the belief, derived from supply and demand analysis, that the government borrows from the private sector when it runs a deficit, and that, therefore, a deficit reduces total savings.

Here’s the way that Mankiw’s Macroeconomics textbook puts it: there’s a stock of money that people have saved—shown by the line labelled S1. A government deficit takes some of that, leaving less for investment by the private sector—shown by the line labelled S2.

Mankiw explains that the move from S1 to S2 is caused by government spending exceeding taxation:

the government finances the additional spending by borrowing—that is, by reducing public saving. With private saving unchanged, this government borrowing reduces national saving. As Figure 3-10 shows, a reduction in national saving is represented by a leftward shift in the supply of loanable funds available for investment… the increase in government purchases causes the interest rate to increase and investment to decrease. Government purchases are said to crowd out investment. (Mankiw 2016, p. 73)

If this were true, then it should be easy to show by looking at bank accounts, since the vast majority of our savings today is in the form of bank deposits, rather than cash. Even if you’ve put your own money into stocks and bonds, that money is still in bank deposit accounts: it’s just in the bank deposit accounts of stockbrokers and pension funds, rather than your own.

Mankiw claims that a government deficit moves the savings curve to the left: it reduces Deposits. A government Deficit is the difference between government spending and taxation, and both spending and taxation operate through bank deposit accounts. Government spending increases bank deposit balances; taxation reduces them. So, what happens when the government runs a deficit; what happens when government spending exceeds government taxation? Bank deposits rise: a deficit doesn’t reduce the stock of savings, it increases them.

In other words, Mankiw’s textbook (and all other mainstream economics textbooks) moved the supply curve the wrong way: he should have shown that the deficit increases savings.

Why does the textbook get it wrong? Partly because the supply and demand diagram is just a drawing: you can draw a line on it anywhere you like. To know where you should draw the line, you have to know how whatever you’re talking about—be it breakfast cereal or money—is created. Mankiw might ultimately be right in his claim that government borrowing imposes “an unjustifiable burden on future generations” (Mankiw 2016, p. 557), but you’ll never know by drawing lines on a diagram. You have to look at how money is created—and that involves the potentially dry and boring topic of double-entry bookkeeping, which I’ll discuss in the next post.

Mankiw, N. Gregory. 2016. Principles of Macroeconomics, 9th edition (Macmillan: New York).

Good, lets get to accounting and where utilizing its money creation and distributional effects a monetary policy will have most beneficial macro-economic effect. Thats the point of retail sale...which EVERYONE either participates in or is effected by, making such policy a new aggregative macro-economic insight that has been going on hundreds of millions of times every day for centuries if not millenia and has been waiting for us to cognite on.

That specific policy is a (at least) 50% Credit/Debit policy at retail sale. Immediate effects: beneficial price and asset deflation, doubling of everyone's purchasing power, potential doubling of demand for enterprise' goods and services and last but most importantly transforms the economic process from a continuously aggravating experience into the greatest opportunity to self actualize gratitude since meditation and prayer. Thats what I refer to in my book as a mega-paradigm change.

Extend accounting's power to a 50% Monetary Gift to the bank/Debt jubilee to the individual policy at point of loan signing and now that $500k house you agreed to purchase for $250k at retail sale is reduced to a loan of $125k. Toss in a $1000/mo. universal dividend that enables the elimination of payroll taxes for welfare, unemployment insurance etc. and every employee and every employer's self interests are integrated against "the roving cavaleers of credit" and we might be able to have a capitalistic revolt of the bourgeisie" that Marx fantasized about but didn't have the right policy and technological capabilities to utilize like we have now. Over consumption? What if you had a policy of a sliding scale required percentage of gifted money into 5-6% Eco/Energy R & D/Other Rational Pursuits Treasury bonds. Such a tax is still a monetary gift. Transformation, an aspect of paradigm changes and of the the natural philosophical concept/experience of grace/graciousness.