The meme that is destroying Western civilisation Part VIII

If the government isn't in negative equity, then the private sector is

In the last post (Substack; Patreon), I showed that a government creates fiat money by going into negative financial equity. This creates an identical magnitude of positive financial equity for the non-government sector.

This may strike you as a bad thing: shouldn’t the government strive to be in positive financial equity? The idea that it’s morally repugnant for a government to get into a negative financial equity position by “spending more than its income” is, I think, the major reason why politicians and journalists obsess about balancing the budget, and running surpluses to reduce the level of government debt (I’ll tackle the issue of government debt in a future post in this series).

There are three things wrong with this attitude:

· the logic of double-entry bookkeeping;

· the history of government attempts to get out of negative equity; and

· the existence of nonfinancial as well as financial assets.

If there is either no government sector—or if the government scrupulously equates its spending and taxation, so that it never runs a Deficit, and its financial equity is zero—then the Private Non-Bank Sector of the economy (households and firms) must be in negative financial equity. This is because:

a) since one entity’s financial Asset is another’s financial Liability, the sum of all Assets and Liabilities is zero; and

b) since the Banking Sector must, by law, be in positive Equity (a bank whose short-term Liabilities exceed its short-term Assets is bankrupt), the remainder of the economy must be in identical negative equity relative to it.

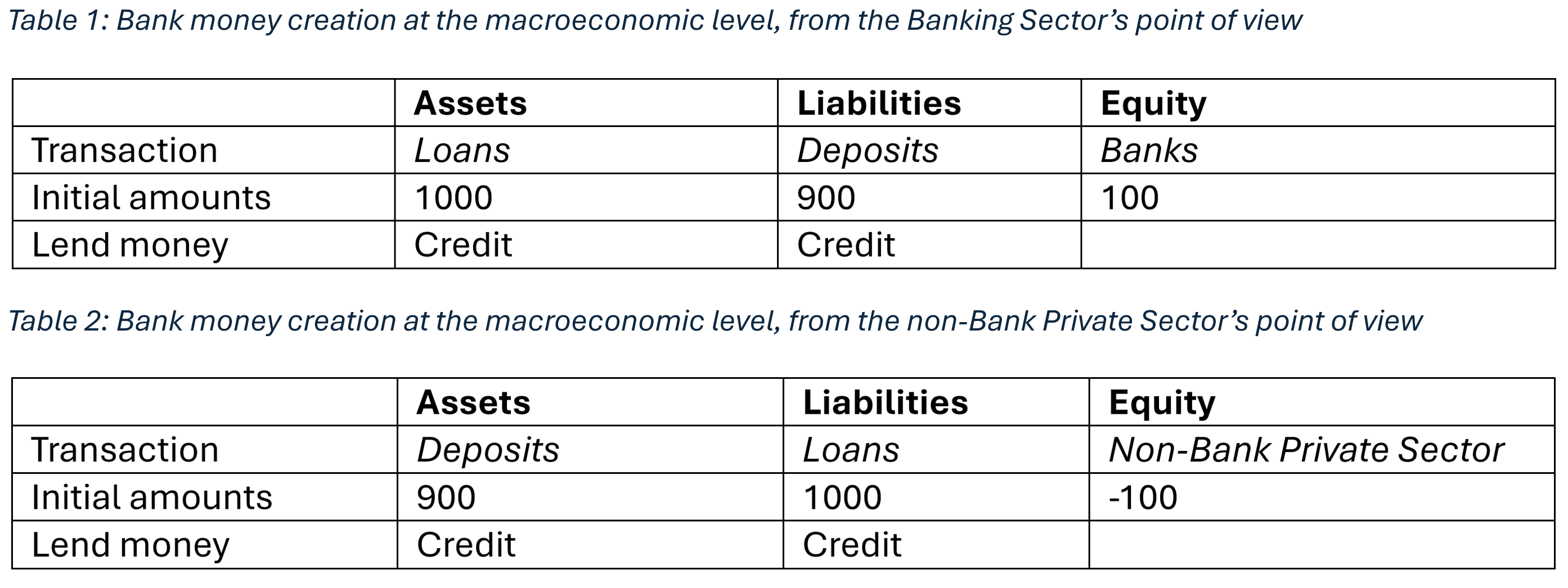

This reality is illustrated in Table 1 and Table 2, which are copied from the 5th post in this series (Substack; Patreon). Since the Banking Sector must, by law, be in positive equity, in a pure-credit economy, the non-bank Private Sector must be in negative equity of the same magnitude. The belief that the government should be in positive financial equity is inescapably also the belief that the non-bank private sector should be in negative financial equity.

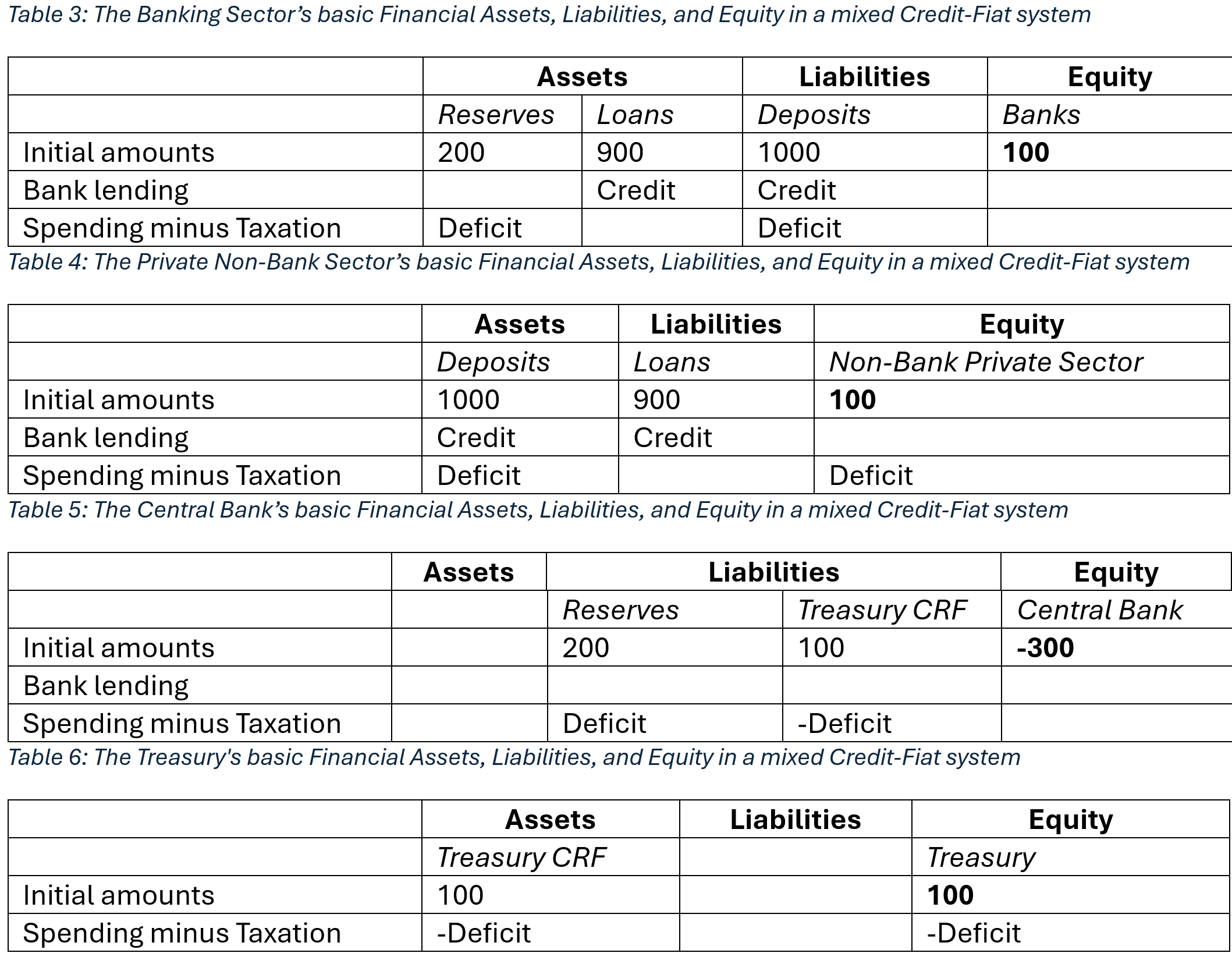

On the other hand, if the government is in negative financial equity, then it’s possible for the non-bank private sector to be in positive financial equity. This is shown in Table 3 to Table 6, which are copied from the 7th post in this series (Substack; Patreon).

Does the moral case for a debt-free government sound so compelling now? I hope not.

It is possible for the private sector to function in negative equity, so long as the income earnt from the turnover of borrowed money exceeds the interest payments on it. But it’s uncomfortable, and it probably goes a long way to explain the historical record that periods of intense speculative activity by the private sector coincided with times when the government ran surpluses and reduced its outstanding debt. Economic busts, and indeed Depressions, followed soon after.

I’ll cover the tragic empirical record of governments attempting to get into positive financial equity in the next post in this series.

Free subscribers: if Substack’s $5 a month is too much, consider supporting me via Patreon for as little as $1/month or $10/year: https://www.patreon.com/ProfSteveKeen.

Makes perfect sense. The only "problem" is how does one best macro-economically/agent aggregatively prevent inflation? To whit, the 50% Retail Discount to consumers and equal Government Rebate back to the merchant granting it to the consumer. The equal debits and credits sum to zero and the result is BENEFICIAL price and asset DEFLATION for both consumers and commercial agents, the end of the banks' monopoly monetary paradigm for the creation and distribution of new money AKA Debt Only and last but not least the transformation of the economy from an unpleasant to onerous experience into the greatest opportunity to self-actualize gratitude since meditation and prayer.

Thats whats called a mega-paradigm change.