Budget Repair? Better to repair your thinking instead

Budget Repair? Better to repair your thinking instead

It's not a good look when your first statement as Treasurer contains a glaring factual error

In his Ministerial Statement on the Economy on July 28th, the new Australian Treasurer Jim Chalmers stated that "the debt burden left to us" is "the highest level as a share of the economy since the aftermath of the Second World War". Oh no it isn't!

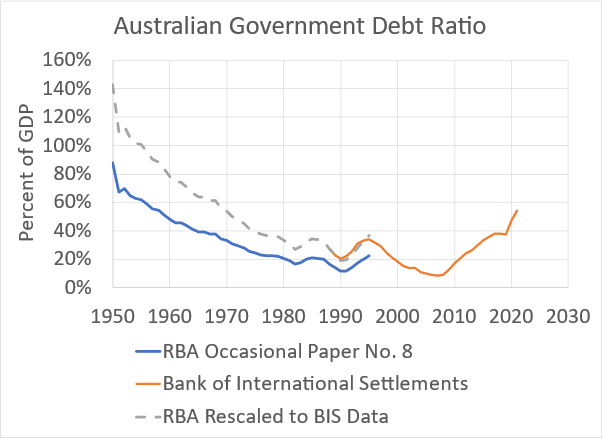

It is the highest level since 1988, in the quarterly data published by the RBA and the BIS (Bank of International Settlements). But a few minutes' browsing on the RBA website will locate Occasional Paper No. 8: Australian Economic Statistics 1949-1950 to 1996-1997, in which annual data shows that the government debt to GDP ratio was 88% of GDP in 1950. This is more than 1.6 times today's ratio of 54%, and that is using a measure of debt that is smaller than the one used today—notice that where they overlap, the blue line for the 1949-1997 lies well below the orange one for 1988-2022.

Rescaling the old data series to match the new where they overlap gives a debt level in 1950 of 143% of GDP, using today's measurements. This is almost three times today's government debt ratio—see the dotted line in Figure 1.

Figure 1: Australia's government debt to GDP ratio since 1950

Chalmers' error is probably the result of lazy research by his staff, rather than by Chalmers himself. But correcting it raises an important question: if government debt was much higher under Menzies than it is today, then is high government debt necessarily a bad thing?

After all, the economy was in a state of near permanent boom under Menzies: the average unemployment rate between 1950 and 1966 was 1.9%, and its peak level in 1961 was 3.2%.

Furthermore, the post-WWII period of strong and tranquil growth ended in 1974—at much the same time that government debt levels fell below the level they've now regained, thanks to the pandemic.

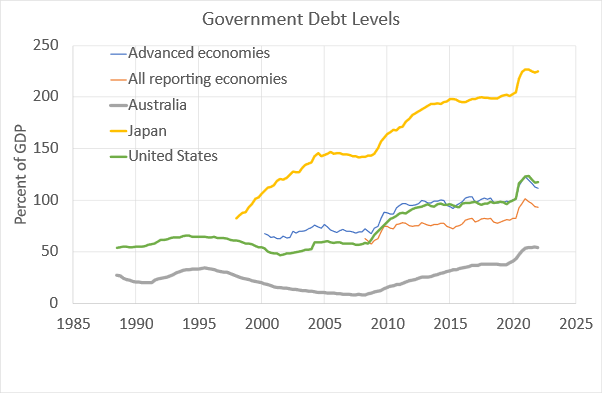

Finally, Australia's debt level, which Chalmers paints as terrifying—"a trillion dollars of debt that will take generations to pay off"—is in fact well below the global average as a percentage of GDP, and less than half the average for advanced economies and the USA. It is barely a fifth of Japan's debt ratio, and, last time I checked, Japan hasn't yet filed for bankruptcy.

Figure 2: Australia's government debt is far lower than the average

So, is it possible that it's not high government debt that is wrong, but our thinking about it?

To answer this question, we'll have to think a lot harder than Chalmers and his staff did, and look very carefully at what government debt is, and what it does. This work starts off boring, and it is a hard slog. But the payoff is that, once you've worked through it, you will realise that everything Chalmers said about government debt and deficits is wrong—and that's a good thing.

The Basics

OK, the boring stuff first: you're going to have to think like an accountant.

Rule One of accounting is that all financial claims are classified as either Assets or Liabilities: a financial Asset is what someone else owes you; a financial Liability is what you owe to someone else. The gap between your Assets and your Liabilities is called your Equity, and of course you'd like that to be positive, wouldn't you? (The correct answer is Yes—but there's a catch).

Rule Two is that every transaction must be recorded twice, in what is known as Double-Entry Bookkeeping. This enables a check that every transaction has been entered correctly. If it is, the verbal equation above—that Assets minus Liabilities equals Equity, which accountants express as —will hold. If it doesn't, you've made a mistake.

Rule Three is that you're going to have to read lots of Tables.

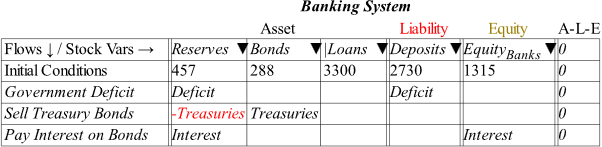

The first table looks at the economy from the perspective of the banking system. To Banks, the money you have in your Deposit account is a Liability; Assets for the Banks are things like Loans, Treasury Bonds, and Reserves; their Equity is the gap between the two. These are the columns of Table 1. The amounts shown in the "Initial Conditions" row is very roughly based on the RBA's data for bank assets and liabilities today.

Table 1: Government spending and taxation from an accountant's point of view

Feeling sleepy yet? Let's see if I can wake you up.

A Deficit creates money, a Surplus destroys it

Table 2 shows government spending and taxation: government spending ("Spend") increases the public's deposit accounts, while taxation ("-Tax") reduces it. If government spending exceeds taxation, so that the government runs a deficit, then the government creates money—and that money turns up in your bank accounts. So, a government deficit increases private sector savings.

Table 2: Government spending and taxation

This is the exact opposite of what economists claim. They allege, to quote a popular first year economics textbook, that "When its spending exceeds its revenue, the government runs a budget deficit, which represents negative public saving" {Mankiw, 2016 #6107`, p. 253. Emphasis added}. Nope, that's flat-out wrong: a government deficit increases public bank accounts and therefore is positive public saving.

Why do economists get this wrong? Because, when it comes to money, they're even lazier than Chalmers' research staff. They simply assume that money doesn't matter in macroeconomics, so they have never properly checked the accounting of money.

When they do try to think about money (yes, that's right, mainstream economists prefer not to think about money), they use their favourite tool, the "supply and demand" model. They assume that a government deficit adds to the demand for money, without changing the supply, and therefore they think the government takes money from the private sector when it runs a deficit.

In fact, as Table 2 shows, a budget deficit increases the amount of money the private sector has: it increases the supply of money, rather than the demand. What a deficit does do is increase the demand for physical resources as there is more money in the system, which people then use to buy more stuff.

The flip side of this is that a budget surplus—a "negative deficit", when Taxation exceeds government spending—destroys money, and reduces the demand for physical resources as there is less money in system to spend.

Note also that the deficit increases bank by precisely as much as it increases . This is important in the next step, government borrowing.

Government debts ain't debts

The way the government borrows is by selling bonds—Treasury Bonds, often called ""—to the banking sector. The government then pays interest on those Treasuries—see Table 3 where I've also combined Government into a single line of Government .

How do the banks pay for these bonds? They use their Reserves. And it just so happens that Reserves have risen because of the Deficit. Therefore, the funds banks use to buy the bonds are created by the Deficit itself.

Table 3: Bond sales and interest payments

I say "funds" there rather than "money" because, though the deficit creates exactly as much in Reserves as it does in Deposits, the banks aren't free to spend these funds: instead, they're effectively holding it in trust for their depositors.

The banks can, however, use those funds to buy Treasuries.

Why should they do this? Because as noted above, they can't spend Reserves, and Reserves earn no interest (most of the time). But Banks can buy Bonds with those Reserves, and Bonds earn interest, and they can also be traded. It would be a brain-dead, non-greedy bank executive that turned down this offer. I can think of some who classify on the first criteria, but I don't know of any with both attributes.

Therefore, the sale of Treasuries isn't so much borrowing from the banks, as an asset-swap that favours the banks. Is that really borrowing, as you and I experience it?

For instance, a mortgage involves pledging your house as security to the bank, in return for which the bank gives you a lump sum, so long as you promise to pay a continuous stream of interest and principal until the lump sum is repaid. If you can't keep your promise, you lose your house.

But what's going on here is more like this hypothetical situation: I give you one trillion dollars, but tell you that you can't spend it, because you're holding it on trust for someone else. Then I say that you can use that trillion to buy certificates off me, on which I'll pay you $30 billion in interest every year, and you can spend that as you wish.

Have I borrowed from you? No way! Instead, I've firstly created a safe but "barren" asset for you—Reserves, which can't be traded, and earn no income—and then allowed you to swap this for a Bonds, a safe and fecund asset, which returns 3% per year. I haven't borrowed from you—I've done you a favour.

Why should I—the government—do that? Maybe it has something to do with the fact that you're running the economy's payments system that is critical to the functioning of the economy.

And where does the government get the money to pay the interest on bonds? Simple: it creates it, in exactly the same way that the Deficit creates money, only this time that money turns up in the financial system—in the Banking sector's short-term equity—rather than in the Deposits of the private sector at the banks.

The Bigger Picture

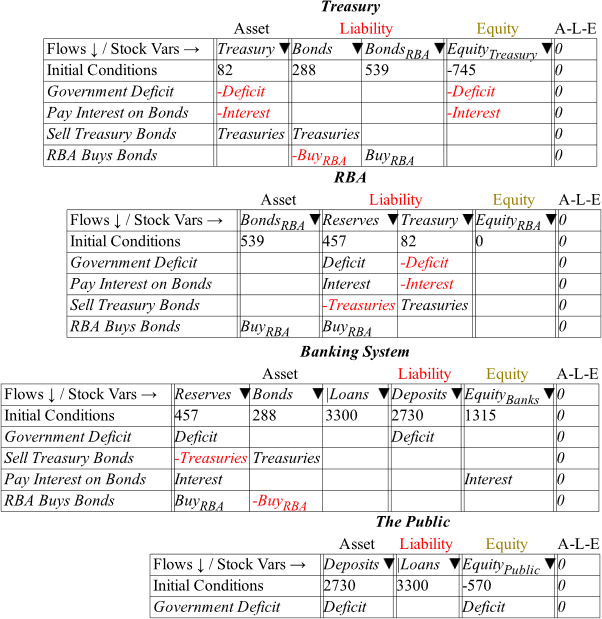

So far, we've just looked at the financial system from the point of view of the Banks. But there are three other perspectives needed to see the whole picture: the Public, the RBA, and the Treasury. Table 4 shows that picture (I've added the RBA buying bonds from the private banks to the mix of activities).

Take a very good look at Table 4, because (a) it matters, and (b) there's a quiz coming up about it.

Table 4: A Bird's Eye view of the entire financial system

So, what did you notice? You should have seen the following details:

The sum of all Equity positions is zero. This is because we're looking at financial assets, which are a claim on other people, and the sum of all claims on other people is necessarily zero;

The Treasury is in negative equity to the tune of $745 billion;

The non-bank Public is in negative equity of $570 billion;

The sum of these two is the mirror image of the positive equity of the banking sector of $1315 billion;

The negative equity of the Government Equity (-$745 billion, the sum of the Treasury [-$745 billion] plus the RBA [$0 billion]) is exactly the same magnitude to the positive equity of the non-Government sectors ($745 billion, which is the sum of the banking sector's positive equity [$1315 billion] and the Public's negative equity [-$570 billion]; and

The flow of negative equity for the Government—the sum of the plus on the —equals the flow of positive equity for the non-Government sectors: the directly increases the equity of the Public, while on the increases the equity of the Banking sector.

What does "budget repair", as conventionally understood, mean from this perspective? It means reducing the negative equity of the government, and therefore necessarily reducing the positive equity of the non-government sectors—the Banks, and the non-Bank public. Clearly, this is not a good idea.

Yes, it may look bad that the government is in negative equity. But once you realise that the sum of all financial claims is zero, the alternative—of the government being in positive equity—would mean that the non-government sector would be in negative equity. Rather than "the government owing money to you", it would be "you owe money to the government". This would have to be borne by the non-bank public, since banks must have positive equity.

Only there would be no money in such a world—or rather, no government-created money. There would still be bank-created money if the government's equity was zero, but that would also be a world in which the non-bank public was necessarily in negative equity, because bank Assets must exceed their Liabilities, otherwise they are bankrupt.

Therefore, government debt, and government deficits, are features, not bugs, of a fiat-money system. Without them, the only money that can be created is created by banks, and this money is offset by an identical amount of private sector debt. Without them, the non-bank public must be in negative equity—given that the banking sector must be in positive equity.

With them, it is possible for both the banks and the non-bank public to be in positive equity—but only if the government runs big enough deficits.

Real budget repair, therefore, means running big enough deficits that the non-bank public can be in positive financial equity.

What about houses and shares?

Notice that, in terms of financial Assets and Liabilities, the non-bank public is in substantial negative equity today. However, there are also nonfinancial Assets—things like a house, which is an asset to its owner, but a liability to no-one (even if there's a mortgage attached to it). The current valuation of Australia's housing stock is 10,000 billion, which lets homeowners and landlords—though not tenants—feel like they're in positive equity.

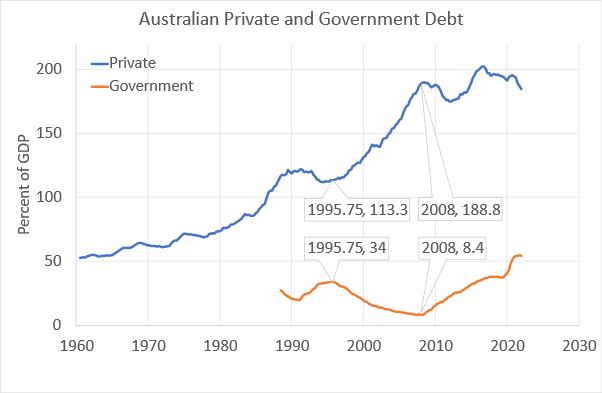

But the monetary value we put upon houses is driven by the amount of money we're willing to borrow to buy them (a topic for another time), and that willingness seems to be driven by how negative our financial equity is. If the government is wrongly obsessed with reducing its own debt, then households seem more inclined to borrow to speculate on rising house and share prices. In a pattern that is repeated in many other countries, the fastest rate of growth of private debt in Australia coincided with the period when the government—specifically, the tail end of the Keating Labor Government and the entire term of the Howard Liberal Government—was crowing about its success in reducing government debt levels. But as government debt fell by about 25% of GDP, private debt rose by 75%. That was not a good trade.

Figure 3: Private debt is more than 3 times the scale of Government debt

Really responsible finance

Chalmers' blooper over the size of the government debt ratio was a useful hook at the start of this article. But that is a trivial mistake compared to looking at the financial sector from only one point of view, the government's, without considering the impact that the government's behaviour has on the non-government sectors, and of treating the government's budget decision as no different to a household's.

These are errors that the Albanese Labor Government, which Chalmers represents, shares with all previous governments—except perhaps that of Menzies himself. As Gareth Hutchens points out, Menzies had no qualms about running a large government deficit, because he understood that a government deficit generates an identical surplus for the private sector. In 1962, a year after he almost lost the 1961 election because unemployment had reached the unacceptably high level of … 3.2%, Menzies out-bid the Labor Opposition's promise to run a £100 million deficit with a promise to:

pay out to the citizens 120 million [pounds] more than will be collected from them… Add to the deficit the tax refunds now being made, and it is clear that purchasing power in Australia this financial year will be uncommonly high. The real task of any government today, as well as of the business community and all sensible citizens, is to get that purchasing power exercised. ("Unlike today's Liberals, Robert Menzies boasted of delivering large budget deficits", Gareth Hutchens, ABC News, 29th August 2020)

Menzies wisdom was born partly of recent experience. The peak level of unemployment under his government, of 3.2%, represented a huge rise from 2.3% the year before, and was caused by a recession which was triggered by an increase in taxes, and a credit crunch. Menzies, Australia's most successful Prime Minister, who governed for sixteen consecutive years from 1949 till 1966, lost 15 seats—over 10% of the House—and won the 1961 election with a mere 1 seat majority.

His flirtation with the false economics of government austerity died with its failure in 1960. Afterwards, Menzies returned to high deficits, and unemployment stayed below 2% for most of the next decade. The deficit added to demand and ensured that the economy remained in full employment.

Menzies learnt from experience, and changed direction. But since him, we have had almost fifty years of policy being dominated by the false belief that the government should have as little debt as possible.

The economy has stumbled, while unemployment remained at treble and more above the level that had been commonplace in the Menzies years. And yet all governments, whether Liberal or Labor, have persisted with the false belief that responsible finance means running surpluses, and reducing government debt—which, in case you've forgotten already, reduces the money supply, and therefore harms economic activity rather than helping it.

Will any of today's politicians, from Jim Chalmers and Albanese's government to Peter Dutton's Opposition, ever come to realise, as Menzies did, that responsible finance means creating enough money to enable the private sector to thrive? And that the austerity they advocate is economically irresponsible?

Frankly, I doubt it.

References

Mankiw, N. Gregory. 2016. Macroeconomics, 9th edition (Macmillan: New York).