Britain Can’t Afford Rachel Reeves (6)

Modelling how Reeves thinks about government spending in Ravel using double-entry bookkeeping

Taking advice from Neoclassical economists about how to control a monetary economy is a bit like taking advice on birth control from The Vatican. Why on Earth would you listen to advice on how to avoid having babies from people who are supposed to not even have sex?

But that’s what Reeves is doing by believing what economics textbooks taught her about government spending. As I noted in a previous post, textbook economics teaches the “Loanable Funds” theory of banking, in which banks don’t create money, but rather act as intermediaries between households—who save money—and firms—who borrow from households in order to invest.

They also teach that governments also have to borrow from households when they government spending exceeds taxation. This extract from Mankiw’s Macroeconomics textbook is typical of the genre (just glance at it, rather than read it—unless you really want to know the equivalent of The Vatican’s advice on sex).

The reason that mainstream economics textbooks are the equivalent of the 1968 Papal Encyclical on birth control is that their models of how money is created are (a) mainly used to justify not including banks, or debt, or money, in macroeconomic models and (b) wrong anyway.

But given how influential these crazy ideas are, I thought I’d try to set out why the textbooks lead Reeves—and her counterparts around the world—to be convinced that, if governments run deficits, then ultimately ruin awaits them: the economic equivalent of an unwanted pregnancy. I therefore built a simple model of “Loanable Funds” in Ravel.

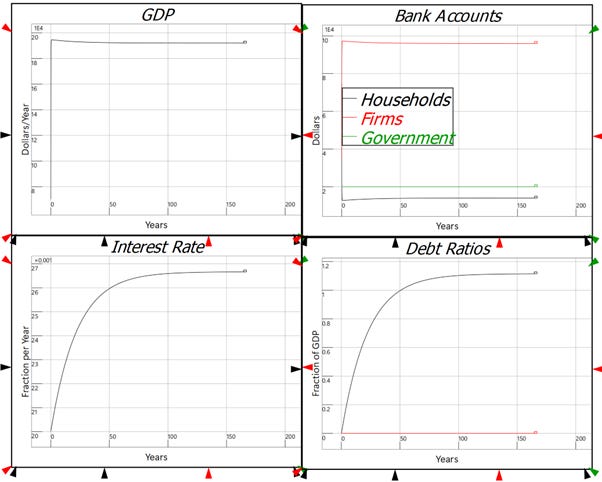

The double-entry bookkeeping table below has the Government, Households and Firms all having bank accounts with private banks. Going through the table line by line:

1. As in economics textbooks, households save and firms borrow from household—that’s the first line in the table;

2. Households lend to earn interest payments from firms;

3. Governments tax households (I’m ignoring corporate taxation for reasons of simplicity);

4. Governments also spend on households—welfare payments, wages, winter fuel subsidies…;

5. The gap between government spending and taxation causes a Deficit, which means that the Government has to borrow from households to cover the gap;

6. Households earn interest income on government debt;

7. To connect households and firms, firms pay wages to households; and

8. Households buy goods and services from firms.

To create a simple numerical model, I have turnover of money in the Firms sector creating GDP, and wages being equal to 70% of GDP:

The supply of Loanable Funds is equivalent to the money in household bank accounts:

Firms borrow from households (for working capital, investment, etc.), where their demand is a negative function of the rate of interest—this simulates the demand curve in the Loanable Funds model:

The most complicated part of the model is that the rate of change of interest rates is a function of net borrowing as a fraction of GDP:

Government spending and taxation are fractions of GDP that are under the control of the Government, but the Government can only spend if it has money in its bank account—“If we can’t afford it, we can’t do it”—so if the government runs out of money, government spending stops (though Taxation continues).

If the government runs a balanced budget, then the stability that Reeves craves ensues (“If we show, as I believe we will, that economic stability is the hallmark of Labour Governments, there is no limit to what we can achieve, because with that stability comes investment. With investment comes growth. With growth comes prosperity.”)

But what happens if the government runs a permanent deficit—in this case, of 1% of GDP? Then you get instability! The government can continue running a deficit so long as it has money in its bank account, but with having to pay interest on its outstanding debt, the trend is for it to run out of money! Then, abruptly, it has to stop spending—though it can still tax. Ultimately this leads to its bank balance becoming positive again, so that it can spend once more—and the unstable cycle repeats. Obviously, we’re better off if the government “balances its books” like a good household, and makes sure that its spending is never greater than its tax revenues.

There’s just one problem with the model of Loanable Funds: its underlying assumptions—that banks don’t lend money (but are mere “financial intermediaries” between Households who save and Firms who borrow), and that Governments also borrow from households in order to spend—are complete bollocks.

In the real world, banks lend, creating credit-based money in the process, while Governments bank with their Central Banks, and therefore create fiat-based money when they spend. I’ll model that reality in the next post.

All of your conclusions are valid of course, but you're not comprehending the deepest problem and hence the earth shaking solution, namely the new APPLIED monetary paradigm concept.

The present monetary paradigm for the creation and distribution of new money is Debt Only. Acculturated since the first day of human civilization its why its so hard for people to understand that government deficits (an aspect of the concept of Debt Only) are actually monetary gifts to the private sector.

Retail sale is the single macro-economic point of the entire economic process. Thus a 50% Discount/Rebate policy at that point doubles everyone's purchasing power and so the potential demand for every enterprise's goods and services, and yet with double entry bookkeeping makes the merchant whole on his entire price, does not cost the merchant a single additional penny and implements beneficial price and asset deflation for EVERY individual. Same equal debits and credits 50% method at point of loan signing continuously integrates debt jubilee into the economic process instead of suggesting a one off ineffective "modern debt jubilee" which sociologically misses the long standing financial and corporate oligarchy. Reforms are shallow and easily over thrown. Paradigm changes totally invert anomalous realities and hence resolve them...until new insights are discovered.

Too much consumption? Mitigate consumption and direct and increase investment with a policy of a sliding scale of required investment of monetary gifts into eco-energy R & D bonds. This tax/cost is still a gift and so philosophically aligns with the new paradigm. And there are other policies to prevent inflation through out the entire economic process using taxation, double entry bookkeeping and monetary gifting.